Die hohe Zeit der Steuerung von Unternehmen mit Hilfe der Kostenrechnung ist vorbei. In den 1960er-Jahren erlebte die Kostenrechnung und damit die Idee ihren Höhepunkt, eine Kostenplanung je Kostenstelle zu erstellen und die Istkosten den Plankosten oder den Sollkosten gegenüberzustellen. Gleichwohl ist die Kostenrechnung (auch Kosten- und Leistungsrechnung oder Kosten- und Ergebnisrechnung genannt) auch heute noch ein wichtiges Instrument des Kostenmanagements und liefert wesentliche Anhaltspunkte für die Preisgestaltung. Mit der Verwendung von SAP-Software in den Unternehmen ist die Integration der Kostenrechnung in die Finanzbuchhaltung und zusätzliche Unternehmensrechnungen vorgegeben. Zudem ist durch die Standardsoftware grundsätzlich die Verwendung einer flexiblen Plankostenrechnung festgelegt.

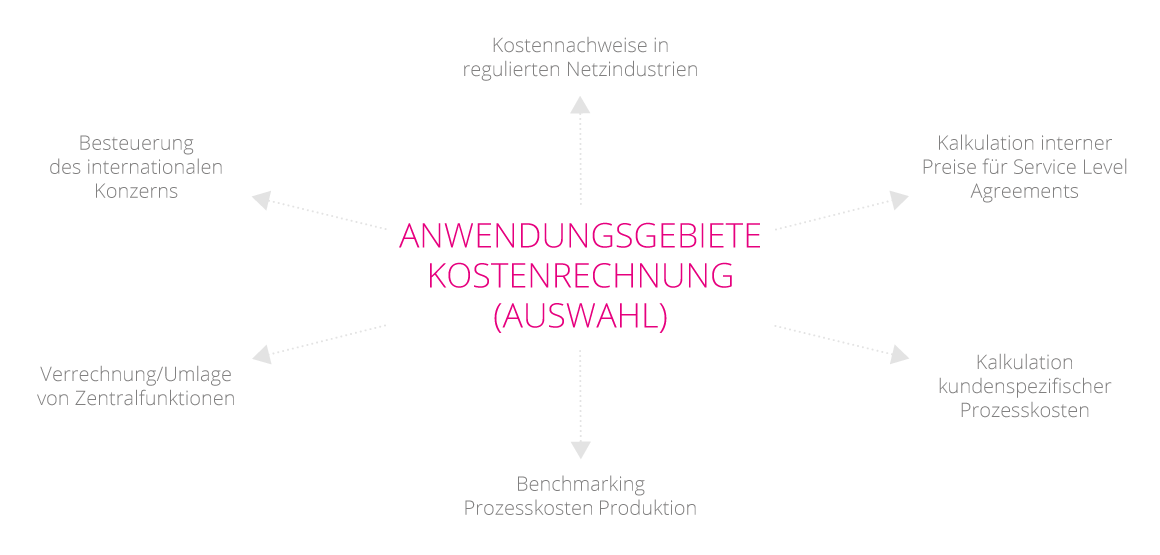

Trotz der geklärten Grundlagen gibt es eine Reihe von Gestaltungshebeln und Kernfragen:

Bei der individuellen Beantwortung dieser Fragen sowie der maßgeschneiderten Ausgestaltung der Kostenrechnung unterstützt Sie CTcon. Wir bauen auf unsere umfangreiche Erfahrung in zahlreichen großen Konzernen. Wichtiger Erfolgsfaktor für die Gestaltung der Kostenrechnung ist die Kompatibilität der Kostenrechnung mit der jeweils spezifischen Ausprägung der Führung und Steuerung des Unternehmens. Bei Bedarf steuert CTcon ergänzend die IT-Implementierung, die entweder durch die Unternehmen selbst oder durch IT-Berater durchgeführt wird.